Intro to Economic Downturns

To understand how to manage our finances during economic downturns, we first need to understand what a downturn is. Broadly, it’s the period in the business cycle when businesses are underperforming and consumers are struggling. More specifically, it’s marked by declines in GDP, employment, and consumer spending.

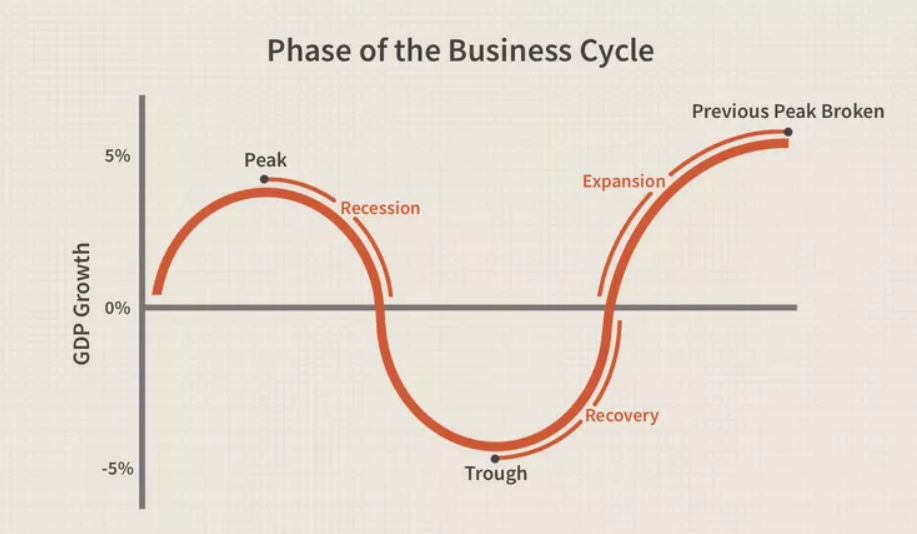

Some downturns are caused by natural shifts in the business cycle (the pattern that economies follow). Essentially, the behavior of both people and businesses are responsive to fluctuations in economic activity – it’s a pattern of overexpansion and contraction, as demonstrated by the image below.

Source: Investopedia

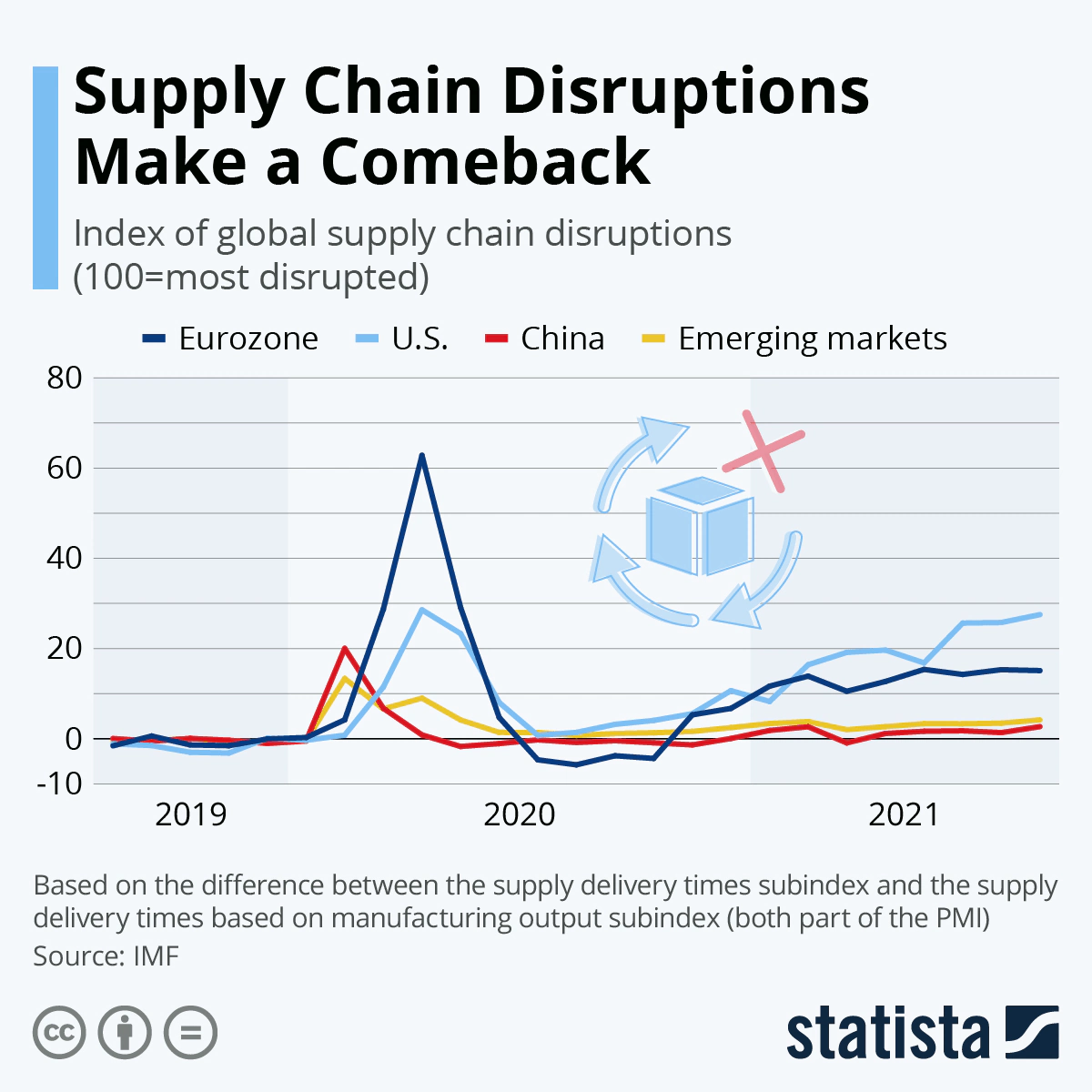

The Dot-Com Bubble in 2001 is a prime example of a business cycle-driven downturn. It was caused by speculative overinvestment (the term “bubble” applies here) in the internet, and a similar phenomenon is likely to occur with AI. The COVID-19 Pandemic, on the other hand, shows how external factors can disrupt supply chains and reduce consumer spending.

Source: Statista

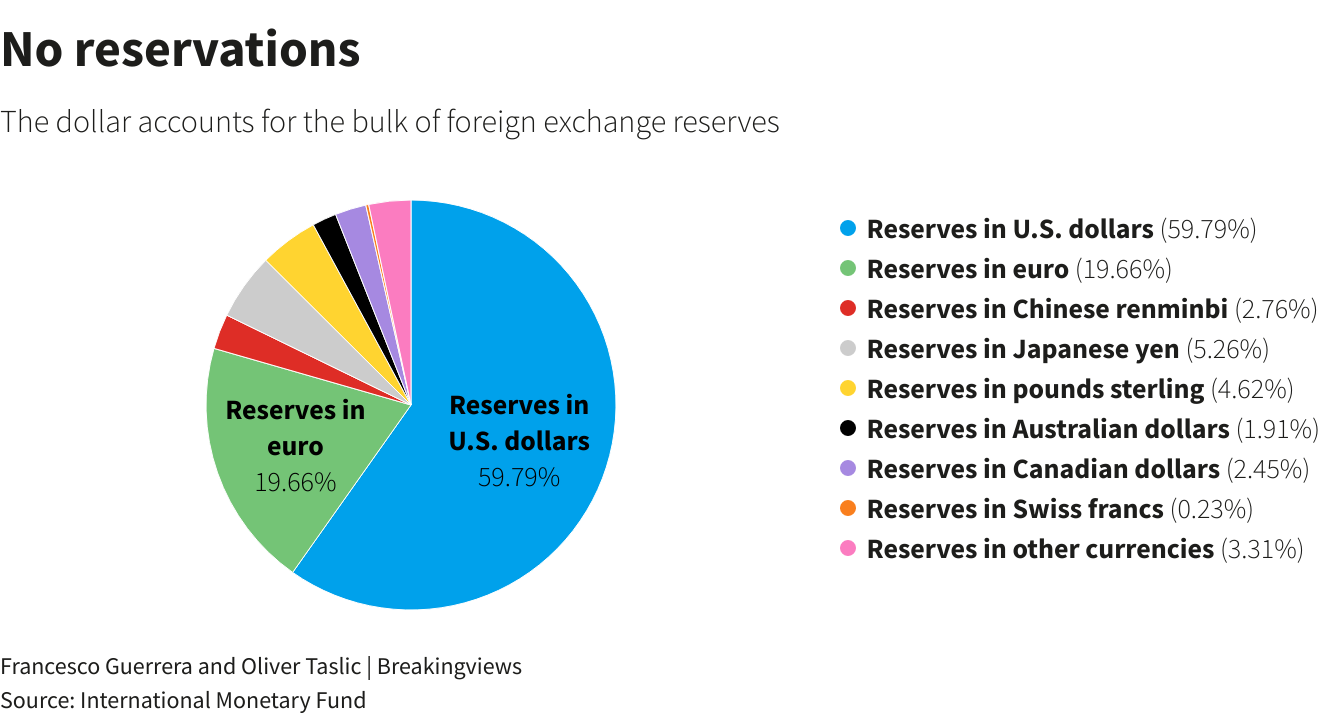

Many other causes exist too. Government policy – from tariffs to to social spending – is a big determinant of how governments and businesses react, which can both benefit and harm economies. And it’s not just domestic – international policy plays a big role. For example, after the US’s Wilson-Gorman Act of 1894, which levied tariffs on many formerly duty-free items, including Cuban sugar, Cuba’s economy (which was reliant on exports to America) fell into a deep recession. Other external factors – from natural disasters to pandemics – can disrupt trade and have profound impacts, which is why it’s important to pay attention to world affairs. But even long-term shifts, such as Japan’s population declining for 15 years in a row, can reduce workforce availability and harm trade. Moreover, it’s essential to understand that we live in a dollar-centric world. That is, foreign currencies are measured in relation to the US dollar, which means that it’s far more likely for a currency crisis to occur in developing countries with volatile markets. The Asian Financial Crisis of 1997, for instance, was caused by Thailand's reserves depleting and currency collapsing because of over-borrowing (banks were eager to borrow to as many lenders as possible to capitalize on interest, but it eventually backfired).

Source: Reuters, using IMF data

Economists classify downturns in multiple different ways. Sectoral downturns, which are usually caused by shifts in demand or overproduction, disproportionately affect specific industries, like housing and coal. The 2008 Housing Crisis was caused by rapid builder development which deflated the value of houses, while the current renewable energy shift will most definitely impact the coal industry negatively. On the contrary, broad downturns have effects on many industries (this is also the distinction between micro- and macro-economics). Some downturns are global. Others are regional. For example, many middle-eastern countries depend on oil from their neighbors like Saudi Arabia and Russia and thus would be harder hit by an uptick in prices in those countries than would the United States (because it has other sources). For this reason, many companies benefit from diversifying their supply chains so that a minor disruption in one part of the world doesn’t halt all production. Simultaneously, it’s also the reason that those who control critical parts of the supply chain hold much power at the bargaining table; look to Egypt and Panama who control the most important maritime trade routes in the world. Then, of course, some downturns are long-term (depression), others are short-term (recession). The short-term ones usually have an immediate cause – like a ship getting stuck in a canal – that can be resolved.

Source: Britannica

Downturns negatively impact individuals, businesses, and governments. Individuals experience decreased purchasing power, job loss, and higher interest rates which put stress on savings and retirement plans and limit their ability to spend on non-essential goods and services, in turn hurting businesses. With reduced revenue, small businesses often go bankrupt while big ones are forced to downsize and let go of workers. This fuels the fire once more: less jobs means less money to spend which means less business revenue which means even less jobs. Governments responsively increase spending on social programs to help those impacted most by downturns, thereby accumulating debt.

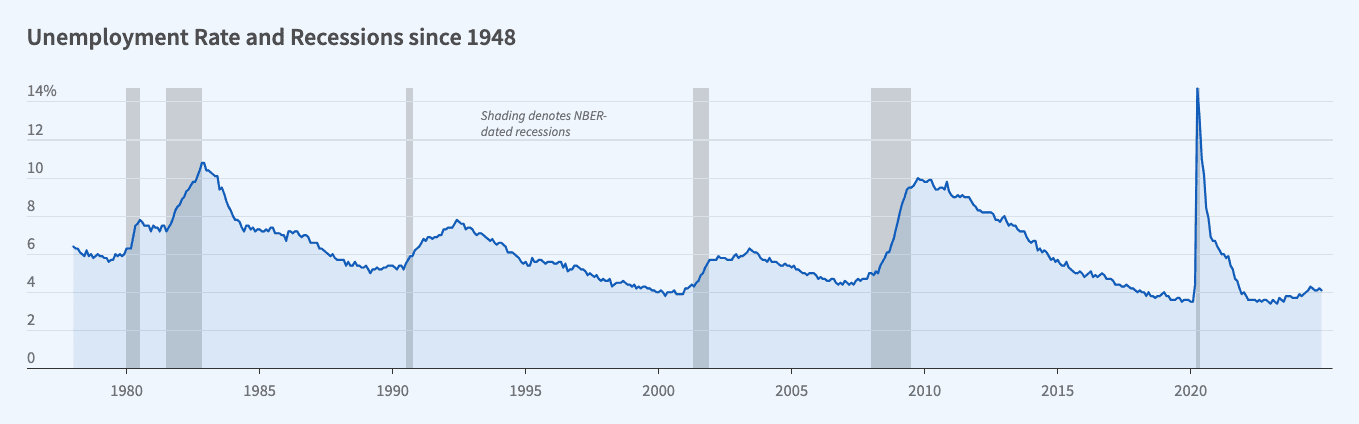

Clearly, we need to prepare in advance to adapt best for downturns, but how do we know they’re coming? The answer is that there’s no straightforward way of knowing when they’ll happen, especially when they’re caused by an external shock (nobody could predict the Pandemic, obviously). But there are early warning signs that economists use to predict downturns caused by business-cycle fluctuations. First, trends in the stock market can indicate the bigger picture. Second, key indicators, like consumer confidence, underperforming might suggest an imminent crash. Third, central bank interest rate (the additional money owed to a lender when a borrower takes out a loan) hikes occur when the government wants to deflate economic activity to avoid a crash, and can tell you a lot about the current economic state. The issue with all of these indicators, though, is that by the time we realize they’re happening, it may be too late, which is why economists have much more complicated means of measuring the risk of recession and often disagree with each other. Our best bet is to stay up-to-date on market trends and signals by following global happenings. An additional tip is that the business cycle generally has a period of about 30 years, though that’s just a trend that doesn’t have a direct causation.

Source: National Bureau of Economic Research

Even though downturns are all but inevitable, financial management is critical. It enables us to protect our wealth, reduce risks, and identify opportunities for growth. The remainder of this course outlines strategies to combat common financial challenges, including greater cost of living and tighter access to credit.