Debt Management

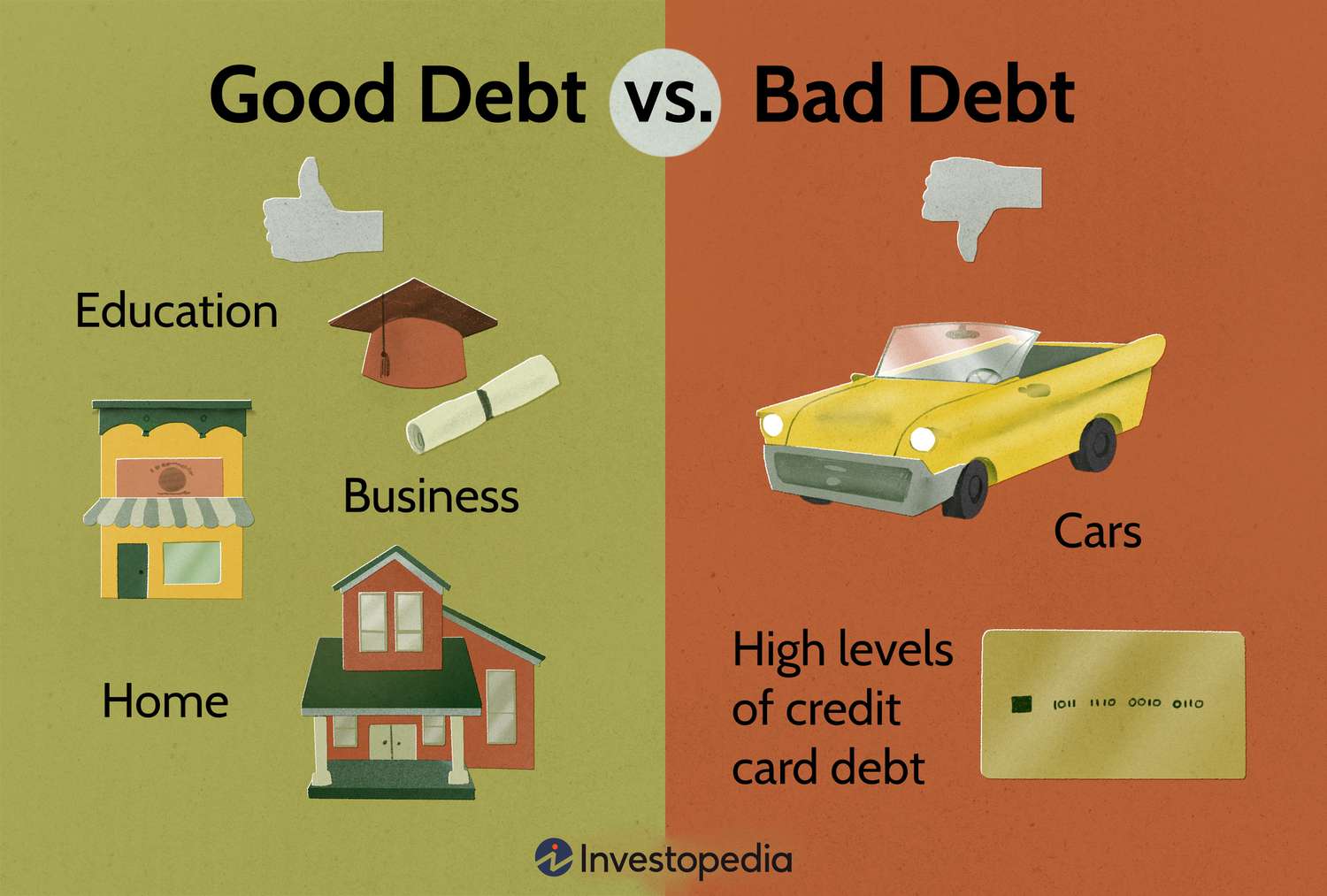

Before we can understand how to manage debt, it’s important to recognize the various types of debt and the implications of taking them on. To start, people often think of some debts sas “good” and others as “bad.” That is, some debts may provide long-term value: a student loan, for example, both invests in your future (those who go to college earn ~$1.2 million more than those who don’t over their lifetimes) and builds credit early (if payments are made on time). An example of bad debt, on the other hand, would be using your credit card to purchase some luxury, non-essential goods that you can’t really afford.

Source: Investopedia

Another distinction in debt is whether or not it’s secured. A secured loan simply means that it is backed by collateral, like a mortgage: if you don’t pay off your debts, the bank will simply take your house away. An unsecured debt has a higher risk to the lender, though, because they don’t get anything if you don’t pay your debt. Take student loans as an example; there is no specific asset that the lender can seize if you don’t pay the debt on time. Because it’s riskier for a lender to loan money that is unsecured, interest rates are often higher for this type of debt.

One last classification to know is the difference between revolving and installment debt. When you think of taking out a loan, you’re probably thinking of installment debt. You’ve borrowed a fixed sum of money, you’re going to pay it back over a fixed period of time, and it likely has a fixed interest rate. Revolving debt, on the other hand, includes something like a credit card. There’s this continuous line of credit that you can borrow from, your repayment is based on how much you borrow, and the loan term has no set period. What you should know about installment debt is that it’s much more flexible but more prone to quick, unexpected changes than the installment alternative, especially when we talk about crisis budgeting (see Chapter 3). That’s why it’s super important to keep track of your various debts in an inventory. For example, you can create a spreadsheet that includes the balance, rate, due date, and lender of all your loans to monitor balances and payoff progress.

In the management process, there are a couple of key metrics to know, the first of which is the annual percentage rate (APR). That’s essentially the annual cost of borrowing money, and it’s usually what credit cards give you. This metric can often be misleading; what you’re actually paying is the effective APR, which takes into account the effect of compounding interest. Make sure to look for that metric when you’re searching for credit cards. The APR divided by 365 is the daily periodic rate (DPR), and it’s certainly important to know because credit cards are compounded on a daily basis. The formula, Interest Charge = (Average Daily Balance) x (Daily Periodic Rate) x (Number of Days in the Billing Cycle), helps you translate between complicated rates and actual money. You can use a card for many different purposes, from standard purchases to cash advances. Many cards offer cashback incentives for certain purchases, so be sure to account for those rewards in the broader context of your typical spending habits when deciding which card is best for you. Importantly, the cash advance rate is always higher than the purchase rate; the cost of borrowing cash from your card is higher than that of simply buying a product. Also, many cards have an introductory APR that is very low for a limited time period – the idea is to hook you in. Watch out for those gimmicks when you’re in the card selection process. Understanding these differences in rates as well as promotional tricks that companies use can help you minimize credit card debt.

Source: Wells Fargo

But no rate is as high as the penalty for when you violate the terms of your initial agreement and pay late, which is why debt management is so important. Remember, every late payment that you make to the credit card company is reported to a credit bureau like TransUnion, Experian, and Equifax, who then collect data on you and report it to other potential lenders. This is where the term “credit score” comes into play: it’s a measure of how good you are as a borrower and gives future lenders an accurate picture of whether or not they should lend to you. Keeping this score as high as possible is important: it’s what enables you to keep acquired interest on loans as low as possible because the bank knows that you are not a risk.

Source: Bayou Mortgage

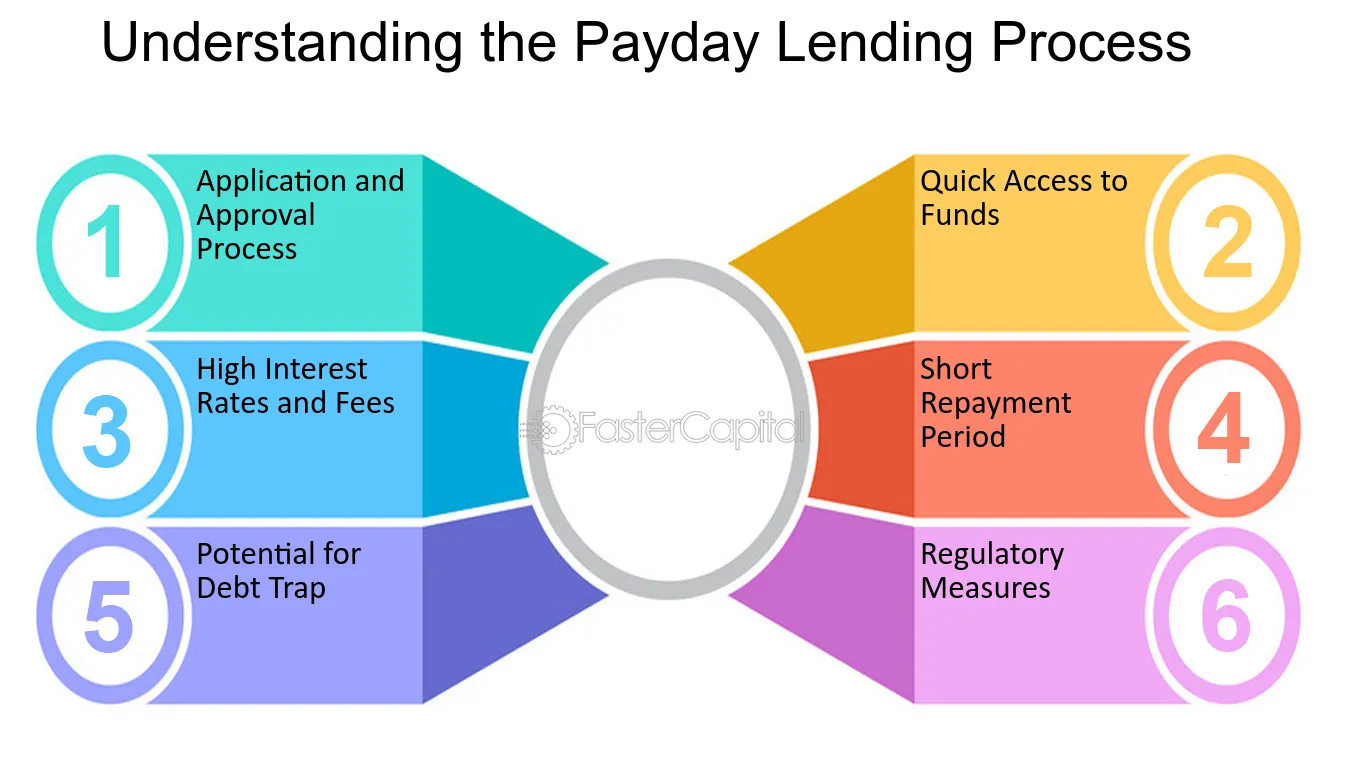

Another way to reduce interest owed is to avoid payday loans. Payday loans are loans of small amounts of money given on the premise that the borrower will repay them when they receive their next paycheck. The issue, though, is that, even though they might be advertised as relatively low interest, they often have high additional fees. Indeed, these loans frequently have exorbitantly high interest rates that are intentionally unsustainable, creating a cycle of debt that forces borrowers to live paycheck-to-paycheck. The only reason somebody would take out a loan like this is if they have an unexpected urgent expense they need to cover, but that’s why the emergency savings fund we talked about (see Chapter 3) is super important.

Source: FasterCapital

Source: myFICO

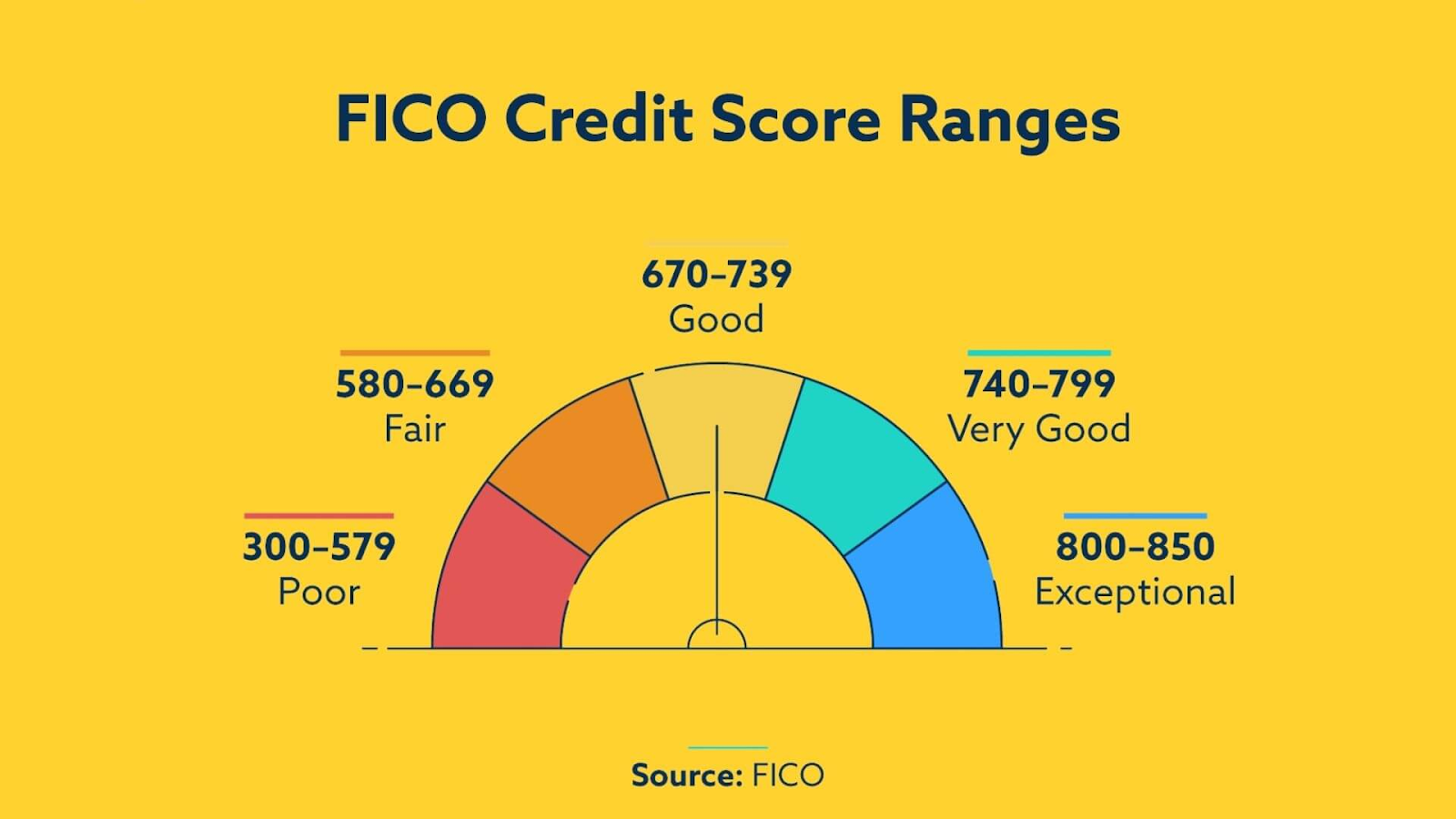

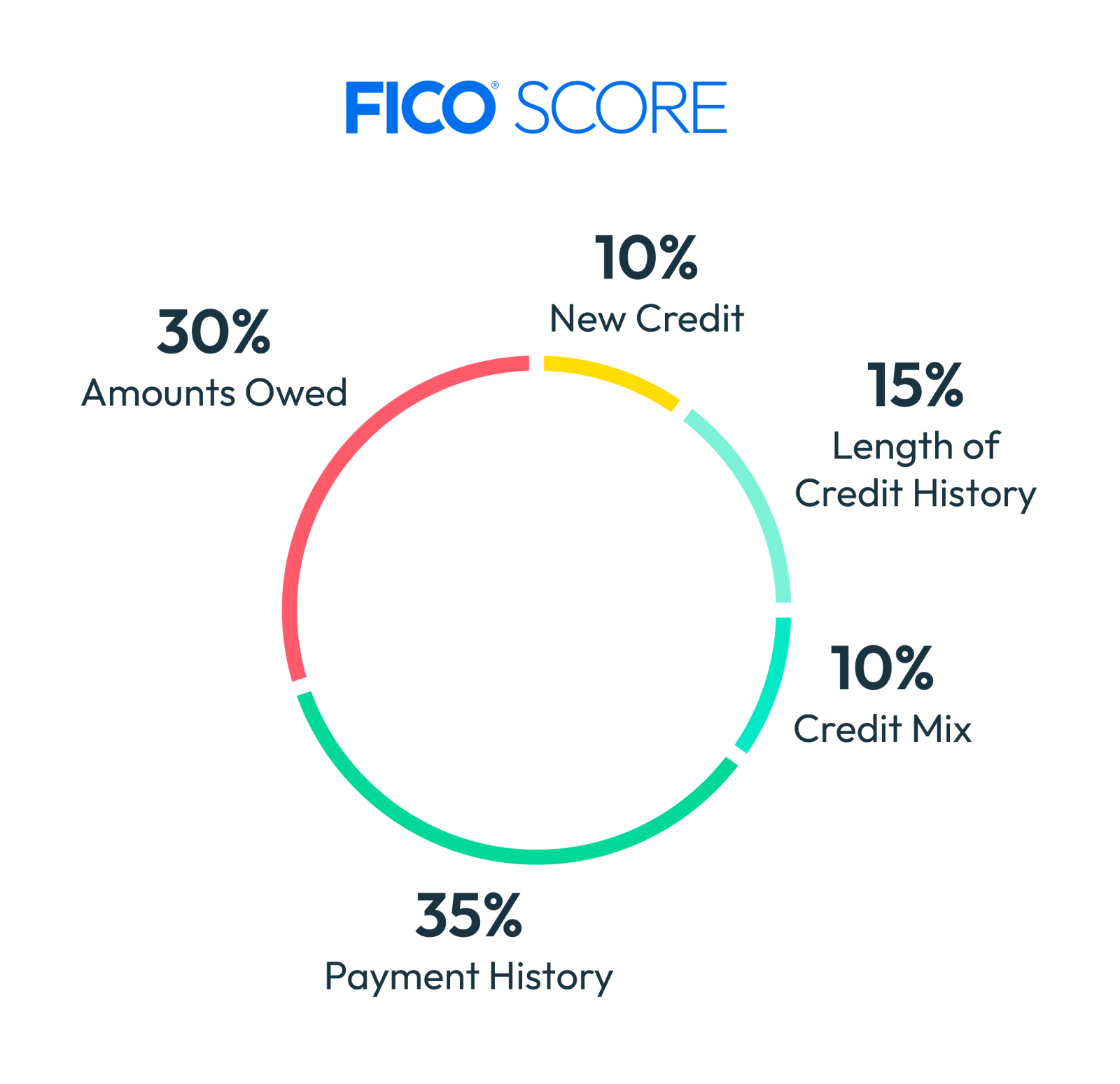

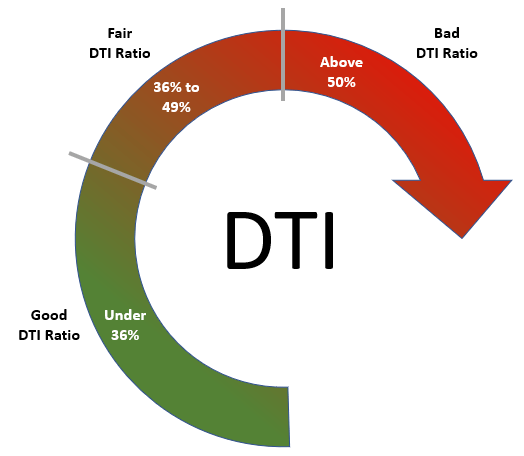

In terms of your credit score (which ranges from 300 to 850), payment history makes up 35% of it, so timely payments are the best way to improve the overall score. But there are other factors. Amounts owed accounts for 30% of your score, and it really relies on your credit utilization ratio. That is, your total credit card balance divided by your total available credit. Keeping this ratio as low as possible is critical. Length of credit history makes up 15% of your score. A longer history positively impacts the score, which is why people often find that taking on manageable debt early is beneficial in the long run. New credit, which is just the amount of recent credit inquiries, makes up 10%. If you’re applying for many loans at once, your score will be negatively impacted. The last factor is credit mix, which just means how diverse your overall lines of credit are. Have many different types – whether it be mortgages, credit cards, or loans – benefits your score. These are all important factors to keep in mind when managing credit. In addition, some lenders use your debt-to-income ratio (DTI), which is exactly what it sounds like, to assess creditworthiness. If possible, keep it below 36%.

Source: Moolanomy

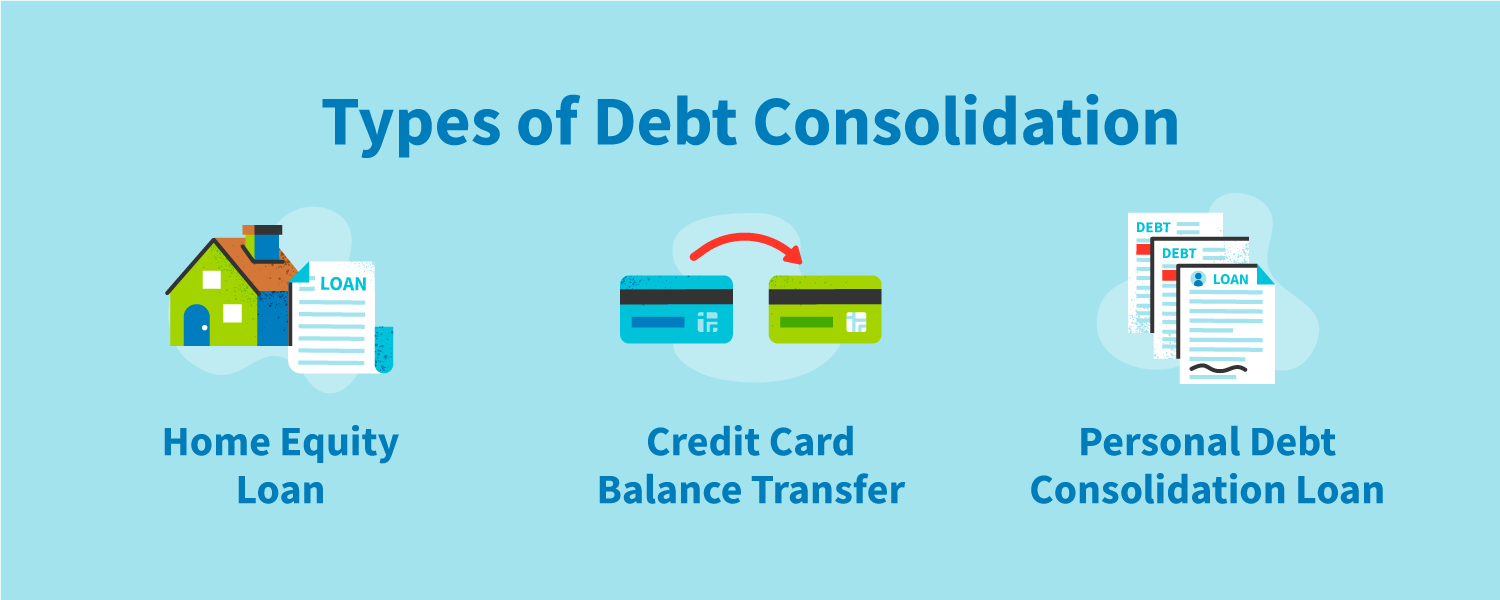

When you have multiple loans in need of repayment, there are two prominent strategies that tell you which ones to pay first. The first is the “high rate method,” which just means that you allocate the most money to the loan with the highest interest rate, which is mathematically and financially optimal. The other strategy, though, is called the “snowball method” which just means that you focus on the debt with the lowest total amount owed first. Using this strategy, you’re going to pay more total interest. However, many people use the “snowball method” because of the psychological benefits that they get from having less loans to pay. Regardless of which strategy you use, you should always have an intention in your debt repayment plan. Oftentimes, plans to combine all of your loans into one exist; this process is known as debt consolidation. However, many people avoid consolidation because they think it results in higher overall interest rates, which is a common misconception. Always do the calculations to figure out what’s more financially optimal or consult an expert. Even if the rate is higher in a consolidated loan, it might be beneficial because, now that it’s just one loan, the likelihood that you forget to pay one of many loans in a given month goes down, reducing any potential harm to your credit score.

Source: Credit Repair

Now that you know how to manage debt, let’s talk about the worst-case scenario: what do you do when you’ve failed? For starters, you can negotiate a debt settlement with your lender. That means that you pay a lump sum of money now (which is less than the total amount owed) to close the loan. While you are technically paying less money than you owe, it’s not great for your credit. You can also file for bankruptcy, of which there are two types. Chapter 7 bankruptcy, or “straight bankruptcy,” is where all of your assets are sold to pay creditors. Chapter 13 of the US Bankruptcy Code, or “reorganization bankruptcy,” is where a new repayment plan is created to pay your lenders back in a more suitable way. While both of these bankruptcies may not sound so bad in theory, they’re terrible for your credit in practice. Chapter 7 will remain on your credit report for 10 years, and Chapter 13 will stay on for 7 years (after you’ve paid the debt back in 3 years). The key takeaway is that you should avoid bankruptcy at all costs.